Data as an asset: Why accounting falls short but is nevertheless becoming inevitable

Data is considered one of the most important assets of modern companies, but it hardly ever appears in most balance sheets. The provocative thesis is that anyone who hopes that a new accounting rule will solve the data problem is confusing accounting with strategy. A data balance sheet can create transparency, but it does not replace an understanding of the economic value of data, let alone the ability to systematically leverage that value.

Key points

- Data is effectively an asset, but largely invisible on balance sheets.

- A data balance sheet would make economic realities more visible, but it does not solve cultural and strategic problems.

- Those who simply wait for new rules to be introduced are wasting time and losing competitive advantages.

Companies between data wealth and balance sheet blindness

In many companies, the current situation is contradictory. Operationally, data is omnipresent; strategically, it is touted as a key resource; but in accounting, it only appears in special cases, such as company takeovers or in the form of clearly defined intangible assets. Industry, trade, financial services and healthcare have enormous data stocks at their disposal, yet annual reports remain dominated by traditional categories such as fixed assets, inventories and financial instruments.

At the same time, US corporations in particular are generating billions in profits with data-based platform models, personalised services and data-oriented advertising and recommendation systems, without the underlying data value being explicitly reported in the balance sheet. Capital markets implicitly price this value in terms of growth, user density and economies of scale. In many European companies, this remains different. Data is fragmented, responsibilities are unclear, data governance appears to be a cost factor internally, and externally, companies appear less innovative than they could be in terms of their data base.

In addition, accounting rules are inherently slow to change. It takes several years to adapt IFRS, HGB or EU directives, and in complex areas, it can take a decade. The economy has long been living in a reality dominated by intangible drivers, while formal regulations are still anchored in the logic of industrial economics.

Key points

- Data is omnipresent in operations, but only visible in the balance sheet in exceptional cases.

- US companies monetise data without adjusting accounting rules, while European companies are wasting potential.

- Regulators are slow to react, while data-based business models are developing rapidly.

The real problem: valuation, use and competitive dynamics

The idea of recognising data as an asset initially seems compelling. Data demonstrably generates income, is similar to intangible assets such as software, patents or customer lists, and is already valued in the context of M&A. Nevertheless, recognising data is not a purely technical addition, but a profound intervention in valuation logic, governance and market mechanisms.

The first major problem lies on the valuation side. The economic value of a data set is context-dependent, dynamic and rarely exclusive. It depends on timeliness, potential uses, the competitive situation, legal restrictions and the company's ability to actually generate products or savings from this data. Traditional valuation approaches such as capitalised earnings, market price or replacement cost are of limited use. In addition, ownership and usage rights are often unclear, especially in the case of personal data or in ecosystems with multiple stakeholders.

At the strategic level, the question is even more relevant: who would actually benefit from a data balance sheet? In absolute terms, US corporations would significantly increase their valuation, as their data-based platform models already contain a high implicit data value. In relative terms, however, European companies could benefit more. They have large inventories from industrial processes, sensor technology, customer relationships and critical infrastructures, the value of which has not yet been systematically measured or communicated in a way that is effective for the capital market.

The decisive weakness of a one-sided balance sheet-oriented view is that it easily becomes a substitute for strategic clarity. Companies run the risk of investing energy in valuations, models and audit processes without really changing their business model, products or decision-making logic. Data then appears as a figure on the balance sheet, not as a malleable production factor.

Key points

- The valuation of data is highly complex from a legal, technical and economic perspective.

- US companies would benefit more in absolute terms, while Europe could catch up in relative terms if it actively uses data.

- Accounting without in-depth use leads to cosmetic accounting rather than genuine value creation.

From the accounting debate to the action agenda: what companies should do now

Instead of waiting for new accounting rules, it is worth asking a sober question: what can companies do today to treat data as an asset, regardless of whether this is already visible in the balance sheet? The economic logic remains the same, even if the formal rules will not change for several years.

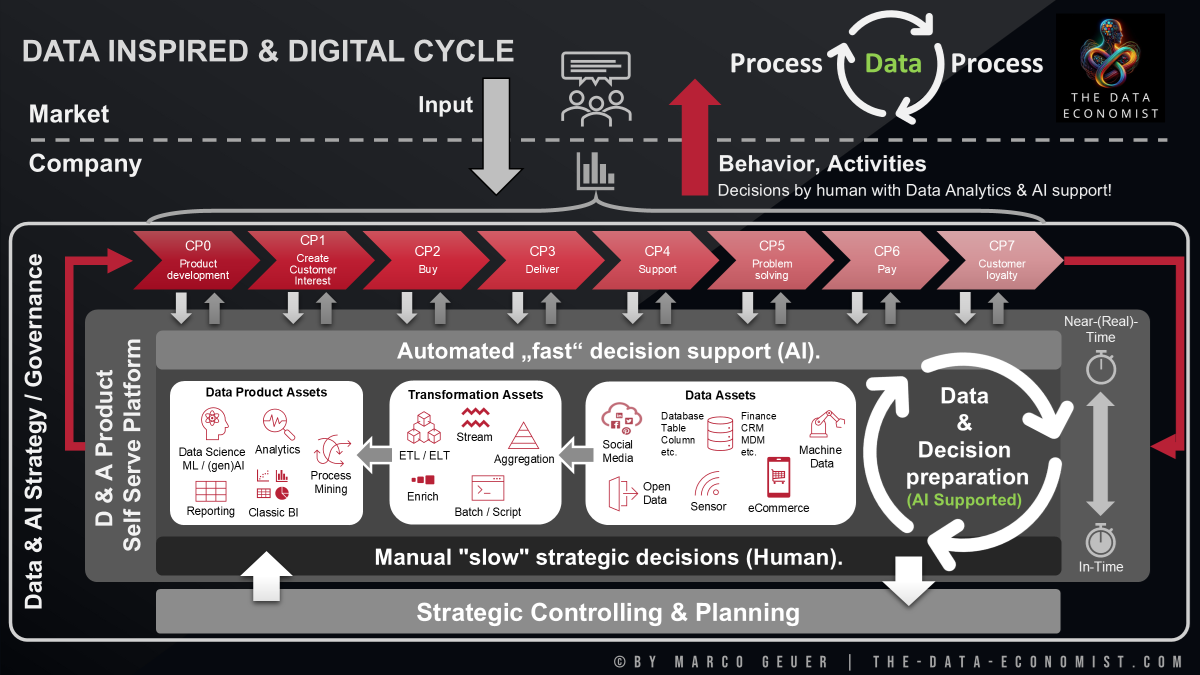

Firstly, companies should consistently treat data as an asset internally. This means a structured inventory of central data sets, a clear allocation of ownership, regular assessment of benefits, risks and quality, and a close link to business strategy. In practical terms, this means identifying critical data objects, documenting their role in central processes and products, and making their contribution to revenue, efficiency or risk reduction traceable.

Secondly, there needs to be a shift from project to product logic. Data products, such as standardised data views, feature stores, customer segments or quality metrics, can be managed like other products with a life cycle. They have defined user groups, quality requirements, service levels and an economic target value. In this model, data governance does not act as a brake, but as a quality framework, comparable to industrial quality management.

Thirdly, the time axis is important. Operational data-oriented improvements generate measurable effects within one to three years. Strategic data-based products and decision intelligence tend to take three to six years. Data sets that are ready for accounting purposes, with robust valuation models and governance structures, take five to ten years to develop. Anyone who starts systematically managing data as an asset today is laying the groundwork for formal accounting at a later date, should this be introduced.

Fourthly, leadership is required. As long as data is treated as an IT issue, it remains tactical. Only when top management understands data as a production factor alongside capital, people and technology and manages it accordingly does a genuine asset logic emerge. This includes incentive systems that reward data quality and data usage, participatory committees for prioritisation and a clear commitment that data competence is a management task.

Key points

- Companies can already manage data internally as an asset, even without a balance sheet obligation.

- Data products and product logic make the value of data concrete and controllable.

- Economic benefits arise in three waves: operational, strategic and balance sheet.

- Without leadership, ownership and incentives, data value remains theoretical.

Conclusion: accounting rules will come, competitiveness will come sooner

Whether and when data will formally become eligible for accounting on a large scale is a question of regulation, lobbying and international coordination. Realistically, such a change will take years. For the competitiveness of a company, this time frame is too slow when data already determines margins, innovation capacity and market access today.

The provocative insight is therefore that the debate about data in the balance sheet is important, but secondary. It reflects how difficult organisations still find it to systematically manage intangible value drivers. The decisive factor is not whether data is listed as an asset, but whether a company is able to generate economic benefits from its data repeatedly and scalably.

A future data balance sheet can make this path visible and improve capital market communication. However, it will only become an advantage if companies have learned by then to embed data in processes, products, decisions and business models. Those who start treating data as a real asset today will benefit from future accounting rules. Those who wait until the rules are finalised will only be able to manage them.

Key points

- Accounting rules for data will develop slowly, but the market for data value is already developing.

- Strategic advantage comes from use, not from formal capitalisation.

- Companies that already treat data as an asset today will be prepared when regulation catches up.

More articles on related topics:

Data as an Asset, Data Valuation, Data Asset Accounting, Economic Value of Data, Data Balance Sheet

- Geändert am .

- Aufrufe: 6487